Regular cash flow forecasts help you keep your focus. If you can't reach your targets for income, reining in your costs may give you a little extra headroom to manage cash flow while you plan your next move. Read More…

By Charles Talbot

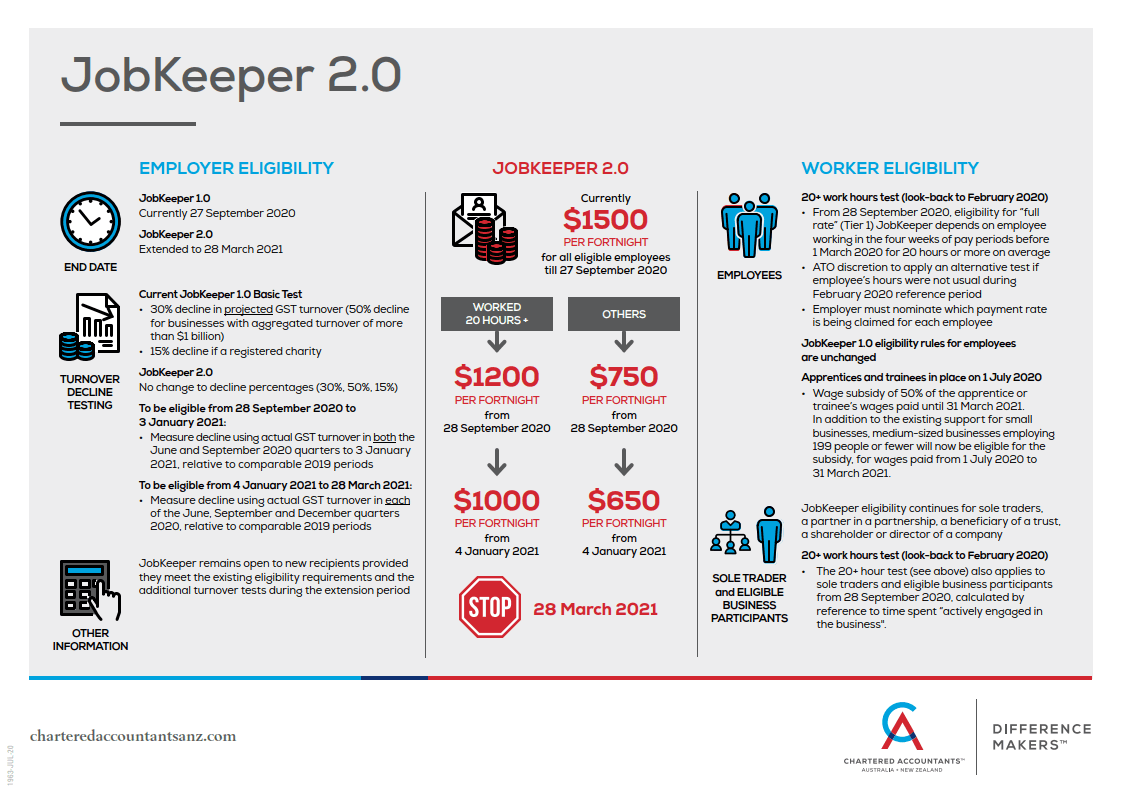

Important changes to the JobKeeper payments from 28 September 2020.

Update: The ATO has updated JobKeeper "2.0". Please see our new blog post on the topic dated 7 August 2020.

The JobKeeper Payment, which was originally due to run until 27 September 2020, will now continue to be available to eligible businesses (including the self-employed) and not-for-profits until 28 March 2021.

The First JobKeeper Payment Extension is from 28 September 2020 to 3 January 2021

To be eligible, businesses and not-for-profits will need to demonstrate that they satisfy the actual GST turnover test in the both the June and September quarter 2020 relative to comparable periods.

Employee eligibility will remain unchanged but the payment rate during this period will be updated to:

Second Jobkeeper Payment Extension is from 4 January 2021 to 28 March 2021

To be eligible, businesses and not-for-profits will again need to demonstrate that they satisfy the actual GST Turnover Test in each of the June, September, and December 2020 quarters relative to comparable periods.

Employee eligibility will remain unchanged but the payment rate during this period will depend on hours the same as above and will be updated to:

Actual GST Turnover Test

To be eligible for JobKeeper Payments under the above extensions, businesses and not-for-profits will need to demonstrate that they have experienced the following decline in turnover:

If a business or not-for-profit does not meet the additional turnover tests for the extension periods, this does not affect their eligibility prior to 28 September 2020.

The Commissioner of Taxation will have discretion to set out alternative tests that would establish eligibility in specific circumstances where it is not appropriate to compare actual turnover in a quarter in 2020 with actual turnover in a quarter in 2019, in line with the Commissioner’s existing discretion. Information about the existing discretion can be found here.

Learn more from Treasury on how this will impact you or your business. Alternatively, please do not hesitate to contact our office on 02 6921 5444.

Director

Regular cash flow forecasts help you keep your focus. If you can't reach your targets for income, reining in your costs may give you a little extra headroom to manage cash flow while you plan your next move. Read More…

How to improve your customer experience as a retail business

Did you know that 84% of customers will walk away from a bad online shopping experience? Here’s what you can do to stop those cart abandonments. Read More…

Federal Budget 2026–27 Proposed Tax Changes – Early Summary (Subject to Legislation)

The Federal Budget was handed down on Tuesday night, announcing a number of significant proposed tax changes affecting capital gains tax (CGT), property investment, trusts, and small business. Read More…